.png)

AWS Savings Plans commit you to a fixed dollar-per-hour spend rate and automatically apply discounts across EC2, Fargate, and Lambda regardless of instance type. Reserved Instances commit to a specific instance family, size, and region for 1–3 years in exchange for deeper but rigid discounts. Savings Plans suit evolving, dynamic workloads. Reserved Instances suit stable, predictable compute with no planned architectural changes.

Bottom line: If your cloud environment changes more than once per quarter, AWS Savings Plans offer safer coverage. If your compute hasn't changed in 18+ months, Standard RIs may offer a deeper discount. If you want commitment-level savings without absorbing AWS's financial risk on either option, Usage.ai's Flex Commitments add cashback protection to the equation and have delivered $91.9M+ in verified savings across 300+ enterprise customers.

AWS Savings Plans and Reserved Instances look like straightforward financial tools. They promise predictable discounts in exchange for predictable usage. But beneath that simplicity lies one of the most misunderstood and financially sensitive subjects of cloud management.

With autoscaling, spot usage, and frequent deployments, modern cloud environments don’t behave predictably. Usage shifts daily, architectures evolve, and engineering teams adopt new compute types long before old commitments expire. That volatility turns multi-year AWS commitments into a forecasting exercise most organizations can’t reliably perform.

This mismatch is the root cause of stranded Reserved Instances, underutilized Savings Plans, and millions in avoidable waste. It’s not that teams don’t want savings; it’s that AWS makes savings dependent on predictions no one can reliably make.

This guide breaks down the full SP vs RI comparison, answers the questions FinOps teams actually ask (including whether you can use both together), and explains how Usage.ai's Flex Commitment and Cashback model introduces a smarter, safer way to capture discounts without absorbing commitment risk.

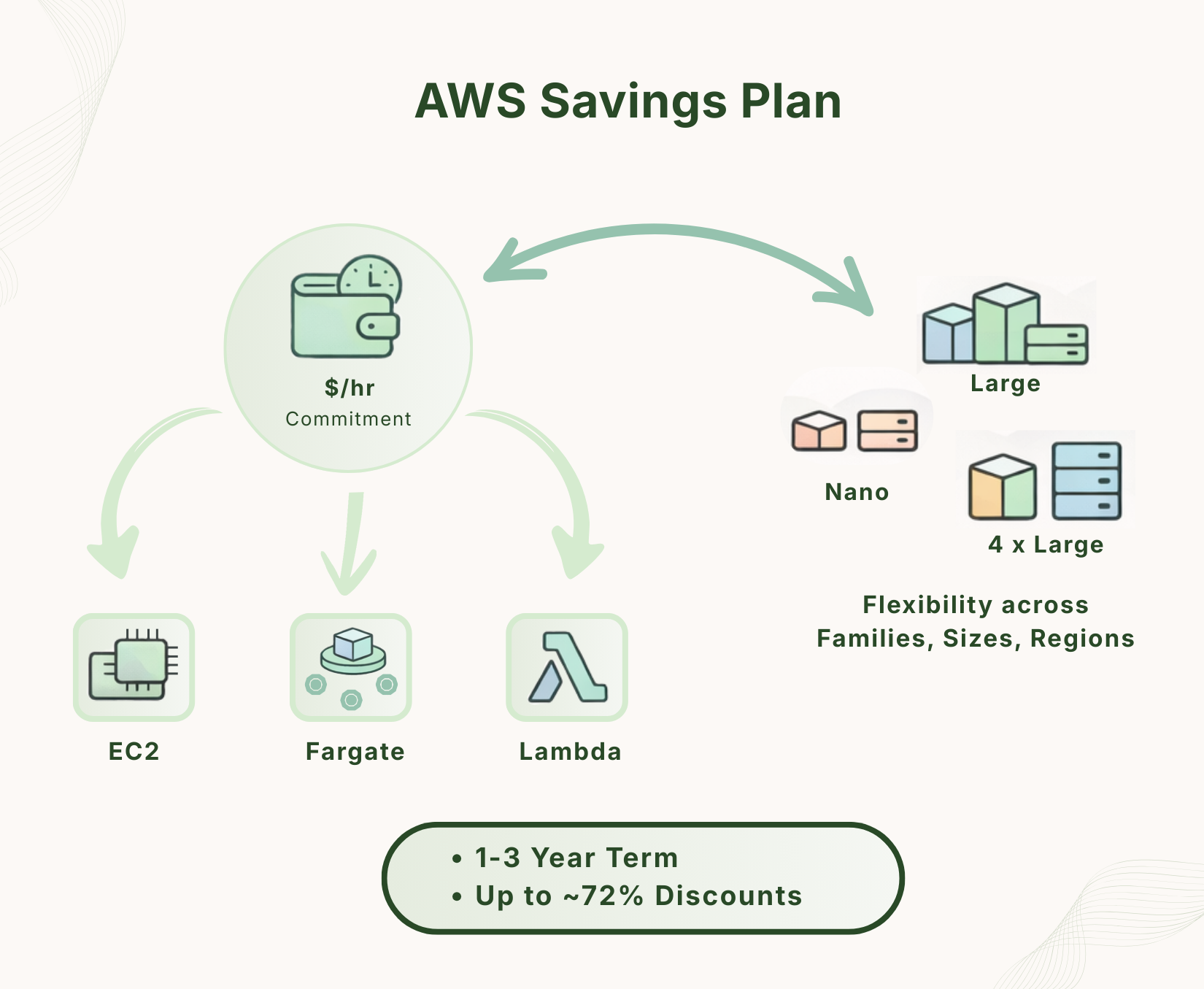

AWS Savings Plans are a flexible pricing model introduced by AWS in 2019 that allows organizations to reduce compute costs by committing to a consistent hourly spend on compute resources over a one- or three-year term.

Instead of committing to specific infrastructure configurations, organizations commit to a fixed dollar amount of compute usage per hour (for example, $20/hour). AWS then automatically applies the discounted rate to any eligible compute usage until the commitment is fully utilized.

If usage exceeds the committed spend, additional consumption is billed at standard on-demand pricing.

This design allows the discount to automatically adapt to changing infrastructure, making Savings Plans particularly useful for environments where workloads scale dynamically or infrastructure changes frequently.

Key characteristics:

When AWS Savings Plans make sense: Dynamic environments, containerized workloads, serverless adoption, frequent instance-family upgrades, or multi-account architectures.

Also read: What is Cloud Unit Economics?

AWS offers three Savings Plan types, each designed with a different flexibility profile:

Compute Savings Plans (most flexible): Apply across all EC2 instance families, all sizes, all regions, plus AWS Fargate and AWS Lambda. If you switch from m5 to m6i, or scale from medium to xlarge, or move workloads to containers, your discounts follow automatically. This is the right choice for teams with diverse or fast-changing compute patterns.

EC2 Instance Savings Plans (slightly higher discount): Apply only to a specific EC2 instance family within a single region (e.g., m6i in us-east-1). They offer a marginally better discount than Compute SPs but require more forecasting accuracy. Moving to a new instance family or region breaks coverage entirely.

SageMaker Savings Plans: For organizations running ML training, inference, and processing workloads at scale, AWS offers SageMaker-specific Savings Plans. These follow the same spend-commitment model but apply exclusively to SageMaker usage. If your team is growing AI/ML infrastructure, model SageMaker SPs separately from your compute commitments. They don't overlap with EC2 or Fargate discounts.

.png)

AWS Reserved Instances (RIs) are a long-standing pricing model that allows organizations to receive discounted compute pricing in exchange for committing to specific infrastructure configurations for a fixed term.

When purchasing a Reserved Instance, organizations commit to attributes such as:

Because the commitment is tied directly to infrastructure configuration, AWS can provide higher discounts compared to on-demand pricing, often reaching up to 75% savings for long-term commitments. However, this rigidity also introduces infrastructure planning risk if workloads change.

Key characteristics:

When RIs make sense: Long-lived workloads, legacy monoliths, stable databases, predictable EC2 fleets where the instance family, size, and region are unlikely to change.

Also read: AWS Budgets vs Cost Explorer: Key Differences Explained

Standard RIs offer AWS’s absolute best EC2 discounts, but they do it by locking you into a very specific instance setup for one to three years. You can’t change families, you can’t resize, and you can’t shift regions. They only make sense when you know the environment will stay exactly the same for a long time.

Convertible RIs offer more flexibility. You can switch instance families or configurations, but only if the new option costs the same or more. That caveat turns many conversions into an upsell rather than a true adjustment. For sophisticated FinOps teams, Convertible RIs can still be a powerful instrument, but the manual overhead of tracking coverage and executing exchanges makes them operationally expensive compared to more automated approaches.

Moving on, AWS also offers two very different behaviors: one designed for flexibility across an entire region, and the other for capacity guarantees in a single Availability Zone.

The difference between Regional and Zonal Reserved Instances determines how easily your RI coverage follows your workloads as they scale, shift, or evolve.

Regional RIs apply across an entire AWS region, which means the discount automatically follows your workloads no matter which Availability Zone they run in. This makes them ideal for modern architectures that lean on autoscaling groups, multi-AZ deployments, or Kubernetes clusters that rebalance workloads dynamically. Because they aren’t tied to a specific zone, Regional RIs adapt naturally to the way resilient, distributed systems operate.

Zonal RIs, by contrast, tie the commitment to one specific Availability Zone and include a built-in capacity reservation. That reservation can be helpful in rare cases where you must guarantee EC2 capacity in a single zone, such as certain high-throughput legacy systems or regulated workloads.

Also read: 18 Proven Ways to Cut 30–50% of Your Cloud Bill

Reserved Instances may be rigid, but they still deliver meaningful value when the environment is stable enough to support them. In the right conditions, RIs are straightforward, predictable, and capable of outperforming Savings Plans, especially when workloads barely change over time.

When fully utilized, Standard 3-year RIs offer AWS’s strongest EC2 discounts. If you already know exactly which instance family, size, and region you'll need for years, RIs can beat Savings Plans on pure savings potential alone.

Some workloads genuinely don’t move around much. These long-lived systems are where RIs shine:

If your team knows the instance family, size, region, and architecture will hold steady for years, reserved capacity becomes a reliable way to lock in savings without daily recalibration.

RIs assume a level of compute stability that is increasingly rare. Modern engineering teams move fast, and even small architectural shifts can cause an RI to stop applying.

RIs fall apart when:

Every one of these events breaks alignment. When alignment breaks, the RI stops covering usage, leaving you to pay for a commitment you’re no longer using.

The biggest hidden cost of RIs is its underutilization, because AWS offers zero protection when RIs go unused.

Here’s the uncomfortable math:

This is why many companies either:

RIs reward perfect forecasting. Unfortunately, real engineering environments rarely behave perfectly.

Also read: Cloud Waste in AWS, Azure, and GCP: How to Eliminate It

AWS Savings Plans were created to solve the fundamental limitation of Reserved Instances: cloud evolves faster than configuration-locked commitments can handle.

Instead of committing to a specific EC2 instance family, size, and region for years, Savings Plans let you commit to a level of hourly spend, delivering strong discounts while accommodating the reality of architectural change.

Savings Plans allow customers to commit to a specific dollar-per-hour spend, for example, $10/hour or $20/hour for a 1- or 3-year term. As long as your usage meets or exceeds that hourly commitment, AWS applies discounted rates automatically.

This spend-based model frees teams from the rigid EC2 configuration constraints that define Reserved Instances.

AWS offers two Savings Plan types, each intentionally designed with a different flexibility profile:

%20vs%20EC2%20Instance%20Savings%20Plans.png)

Also read: 10 Biggest Cloud Cost Optimization Challenges (and How to Solve Them)

Savings Plans solve many of the operational bottlenecks associated with Reserved Instances, making them well-suited for fast-moving engineering teams.

This includes the ability to change instance families, instance sizes, and underlying architectures without invalidating the discount. This can be a requirement in environments that routinely adopt new compute generations or shift across hardware types.

Coverage spans EC2, Fargate, and Lambda (for Compute SPs), giving organizations the ability to mix serverless, containerized, and VM workloads without managing multiple commitment models.

They eliminate the need for conversions, instance-type tracking, and configuration-specific governance workflows, which significantly reduces coordination across FinOps, platform teams, and engineering.

As teams migrate from x86 to ARM-based architectures, Savings Plans follow those changes automatically, preventing discount loss during transitional periods.

Workloads that regularly shift between us-east-1, us-west-2, and eu-central-1 remain covered under Compute SPs, greatly simplifying planning for global deployments.

Even with significantly better flexibility, Savings Plans still fall short in several important areas.

If spend declines because of right-sizing, optimization, or unexpected downtime, the commitment continues billing at the pledged hourly rate, creating the same type of underutilization risk as RIs.

Teams with large traffic swings, such as retail, travel, or streaming may be locked into high hourly commitments during periods of low activity.

If an SP is unused, AWS does not reimburse customers in any form; the financial risk remains entirely on the buyer.

They require a 1- or 3-year commitment, which may not align with modern agile or growth-stage infrastructure planning.

Right-sizing, moving workloads to spot, or shifting to a new architecture may drop spend enough to create underutilization.

Also read: AWS Database Savings Plans Explained for DB Teams

Savings Plans eliminate much of the rigidity that makes Reserved Instances difficult to maintain, but they still require accurate forecasting and carry the same financial risk when usage dips below the committed spend level.

This is why many organizations evaluating AWS savings plans vs reserved instances struggle to determine which option delivers better long-term value. Below is a practical comparison:

Savings Plans commit you to a dollar-per-hour spend level, not a specific machine. This means that if you commit to $20/hour, AWS applies discounted rates to compute usage until your hourly bill reaches that commitment. This model is inherently resilient to architectural change.

Reserved Instances commit you to a specific machine shape, including the instance family (e.g., m6i), instance size (e.g., large), region (e.g., us-east-1), and tenancy. Because these attributes are hard-locked, even small engineering changes can reduce or eliminate RI alignment. This makes forecasting accuracy essential and often unrealistic.

Savings Plans provide high flexibility because they follow your compute strategy wherever it goes. Teams can upgrade to new generations, right-size workloads, adopt Graviton, or deploy across multiple sizes and families without losing discount coverage (Compute SP).

Reserved Instances are low-flexibility instruments. They require workloads to remain consistent for years. If engineering moves from m5.xlarge to m6i.xlarge, or from large to medium, or from us-east-1 to us-west-2, RI coverage may break entirely, leaving companies paying for unused commitments.

Savings Plans cover EC2, Fargate, and Lambda (Compute SP). This is increasingly important as organizations adopt Kubernetes on Fargate, serverless architectures, or a mix of compute surfaces.

Reserved Instances cover only EC2. They cannot discount Lambda, Fargate, or any containerized workloads that move execution layers outside pure EC2.

Savings Plans offer up to ~66% savings, depending on payment structure and term. These discounts are strong but optimized for flexibility over depth.

Reserved Instances can offer up to ~72% savings, especially for 3-year Standard RIs with all-upfront payment. These deeper discounts reflect the rigidity AWS asks customers to accept. But depth only matters if you can maintain high utilization which is the core problem RIs present.

Savings Plans tolerate architectural drift exceptionally well. Changes in instance families (m5 → m6i), sizes (large → xlarge), or compute types (EC2 → Lambda) don’t affect coverage. SPs continue working even when engineering re-architects services, migrates to containers, or modernizes infrastructure.

Reserved Instances tolerate drift poorly. The rigid configuration requirements make RIs highly vulnerable to engineering decisions made outside FinOps. Even small shifts in architecture can eliminate RI coverage and turn commitments into sunk cost.

Savings Plans handle autoscaling patterns perfectly, because they discount the spend, not the machine. Whether your ASG shifts between medium, large, or xlarge nodes throughout the day, SP discounts remain applied.

Reserved Instances are unreliable for autoscaling. If workloads scale into new sizes or if instance types fluctuate, RIs will only apply during the exact window when usage matches the RI configuration. This makes RIs impractical for highly elastic workloads.

Savings Plans require no modifications. There are no conversions, recalibration, or rebalancing. Once purchased, SPs simply apply.

Reserved Instances require ongoing maintenance. Convertible RIs, while more adaptable, still require engineering-heavy calculations and must always be converted into equal or greater value footprints. Standard RIs have minimal modification options and often become obsolete if environments shift.

Savings Plans are ideal for dynamic, evolving environments, including Kubernetes clusters, serverless workloads, multi-account environments, and organizations undergoing modernization.

Reserved Instances are ideal for stable, long-lived workloads, such as legacy monolith servers, static databases, or predictable, unchanging compute shapes. If you know your EC2 footprint will be identical for multiple years, RIs can be attractive.

Savings Plans carry medium underutilization risk, because risk is tied to usage dropping below the committed hourly spend. SPs protect against configuration drift but not usage volatility.

Reserved Instances carry high underutilization risk, because both configuration drift and usage reduction can cause commitments to go unused. This dual-risk profile is why many teams under-buy RIs.

Savings Plans rely on AWS recommendation models that look back over several weeks of usage. Recommendations are generated daily, but they’re based on those longer historical windows, which can make them slow to react in very fast-changing environments.

Reserved Instances face the same issue, since the AWS recommendation engine uses the same multi-week historical data to drive both RI and SP suggestions.

Also read: Cloud Cost Analysis: How to Measure, Reduce, and Optimize Spend

AWS Savings Plans and Reserved Instances share one critical, structural weakness: AWS provides zero financial protection if your usage drops.

If your commitments go unused:

This isn't a design flaw you can engineer around. It's built into the AWS commercial model. Whether you choose the more flexible Savings Plan or the more rigid Reserved Instance, the outcome of underutilization is identical. You pay for something you didn't use, and AWS doesn't give it back.

Yes, and many mature FinOps teams do. The key is understanding how AWS applies commitment discounts in priority order when multiple commitment types are active:

This stacking logic means you can use RIs for your most stable, predictable workloads. For example, a production RDS cluster or a legacy EC2 fleet that hasn't changed instance families in two years, while using Compute Savings Plans to cover the rest of your dynamic EC2, Fargate, and Lambda usage.

However, you still carry two separate underutilization exposures. If usage drops on either commitment type, AWS doesn't compensate you on either.

Below is a step-by-step framework you can use before purchasing any AWS commitment:

Also read: Cloud Cost Monitoring vs Cost Control: What’s the Real Difference?

.png)

Flex Commitments are Usage.ai's alternative to AWS-native commitments. They deliver Savings Plan or Reserved Instance–level discounts while removing the long-term lock-in and underutilization risk that make native AWS commitments financially dangerous for most engineering teams.

Instead of committing to a specific instance family (RIs) or a fixed hourly spend (SPs), Flex Commitments adjust dynamically based on actual usage and include built-in financial protection that AWS never offers.

Think of it this way. AWS's commitment model is like paying 12 months of gym membership upfront, knowing you might only go for six. Usage.ai's model is like paying for the months you actually attended and getting a refund for the ones you didn't.

Flex Commitments are useful in environments with:

Mature FinOps teams evaluate AWS commitments using structured, risk-aware criteria that consider forecasting accuracy, engineering velocity, modernization efforts, and organizational constraints.

The following dimensions are commonly applied when selecting between Savings Plans and Reserved Instances.

Forecasting Accuracy: For predictable usage (±10% over 12+ months), RIs may be viable for specific workloads. Whereas for moderate fluctuation (±20–40%), Savings Plans are safer. For highly variable or unpredictable usage, AWS-native commitments become difficult to size accurately. Flex Commitments remove the risk.

Engineering Velocity: Frequent architectural change, like moving between EC2 generations, migrating from EC2 to Fargate, adopting Graviton, or changing regions reduces RI effectiveness to near zero. Savings Plans tolerate more change but still depend on consistent spend levels.

Modernization Roadmap: RIs generally break during modernization. Savings Plans adapt better but still carry usage risk if spend drops. Flex Commitments are designed for exactly this transition period. They absorb the financial risk that accompanies any architectural change.

Usage Volatility: Seasonal spikes, batch workloads, and shifting demand create underutilization exposure with both native commitment types. Flex Commitments address this directly through cashback on underutilized portions.

Compute Surface Mix: Modern workloads span EC2, EKS, Fargate, Lambda, GPU, and Spot. RIs apply only to EC2 and require alignment. Compute SPs cover multiple surfaces but rely on consistent overall spend.

Governance and Compliance: Neither SPs nor RIs include native approval workflows, cross-account oversight, or change-management compliance. Usage.ai provides all three.

Organizational Risk Tolerance: RIs have the highest risk around configuration and usage drift. Savings Plans have medium risk around usage drift only. Flex Commitments gets you the lowest risk via. cashback protection.

Flex Commitments address many of the risks noted above by removing AWS’s long-term lock-in, refreshing recommendations daily, and offering cashback for unused commitment. They are often evaluated when teams require commitment-level savings but cannot ensure stable configurations, predictable usage, or conservative forecasting windows

Learn more: Which Commitments are Eligible Under the 'Flex-Commit Program'?

There are smarter ways to cut AWS costs than locking yourself into rigid one- or three-year commitments. Usage.ai helps you save more and with far less risk by combining intelligent commitment automation with real cashback protection.

With Usage.ai, cloud cost management becomes refreshingly simple. The platform automatically analyzes your environment, refreshes recommendations every 24 hours, and gives you SP/RI-level discounts without the AWS lock-in. And if your usage dips? You’re protected. Flex Commitments reimburse unused commitment in real cashback, giving FinOps teams the confidence to commit more aggressively without worrying about the downside.

Across 300+ enterprise customers, Usage.ai has delivered $91.9M+ in verified cloud savings with 30–50% reductions achieved within 60 days, zero code changes, and full cashback protection on every commitment.

The platform connects to your AWS environment in 5–10 minutes (read-only access to metadata only), begins cost analysis immediately, and delivers personalized recommendations within 3–7 days. Commitments are never purchased without your explicit approval.

Interested in running a POC? We’d love to show you what safe, automated, cashback-protected savings can look like for your cloud environment. Sign Up now!

1. What's the difference between AWS Savings Plans and Reserved Instances?

Savings Plans are more flexible than RIs and follow your compute usage even if you change instance families or sizes. Reserved Instances are more rigid but can offer deeper discounts if your environment stays stable. Most teams don't stay that stable, which is why both models carry risk if usage drops or architectures change.

2. Are AWS Savings Plans better than Reserved Instances?

For most modern engineering environments, yes. Savings Plans are better when workloads evolve, teams adopt new instance families, or compute spans Fargate and Lambda. RIs are better only when the compute footprint is highly stable and unchanged for extended periods, typically 18+ months. The deeper discount RIs offer only delivers more value if you maintain near-perfect utilization.

3. Can you use AWS Savings Plans and Reserved Instances at the same time?

Yes. AWS applies commitment discounts in priority order: Zonal RIs first, Regional RIs second, EC2 Instance SPs third, Compute SPs last. Many mature FinOps teams use RIs on their most stable workloads and Savings Plans to cover dynamic compute.

4. What happens if I don't use my Savings Plan or Reserved Instance?

AWS does not reimburse unused Savings Plans or Reserved Instances. If your usage drops below your commitment level, you continue paying the committed hourly rate. This is the core financial risk of both commitment types and exactly why Usage.ai's Flex Commitments include real cashback for unused portions paid via ACH or wire.

5. Can I cancel an AWS Savings Plan or Reserved Instance early?

AWS Savings Plans cannot be cancelled once purchased. Standard Reserved Instances can be sold on the AWS Marketplace (with listing fees and no guaranteed buyer), but there's no exit path for Savings Plans or Convertible RIs. This inflexibility is one of the primary drivers organizations turn to Flex Commitments.

6. How much can I save with AWS Savings Plans vs Reserved Instances?

Savings Plans offer up to ~66% savings versus On-Demand pricing. Standard Reserved Instances offer up to ~72% for 3-year, all-upfront commitments. The gap narrows significantly when you factor in underutilization. Note that an RI at 70% utilization delivers less real savings than a Savings Plan at 100% utilization.

7. Why do teams struggle to choose between Savings Plans and RIs?

Because AWS gives you discounts only if your future usage matches a long-term contract. If your usage dips, you still pay for the full commitment. That fear of underutilization leads to chronic under-commitment, even when teams know they could save more.

8. How does Usage.ai help me avoid overcommitting in AWS?

Usage.ai's Flex Commitments give you SP/RI-level discounts without locking you into AWS terms. And if your usage drops, Usage.ai reimburses the unused portion as real cashback, so you never pay for commitments you didn't use.

9. Does Usage.ai provide real cashback or just credits?

Real money. When a Flex Commitment is underutilized, Usage.ai pays back the unused portion via ACH or wire transfer. This is one of the most significant differentiators between Usage.ai and AWS-native commitment tools.

10. Does Usage.ai automatically buy Savings Plans or RIs for me?

No. Usage.ai never auto-purchases anything without explicit approval. Every recommendation goes through a customer-controlled approval workflow so your team stays fully in control of what gets committed.

11. Does Usage.ai work across all AWS accounts and organizations?

Yes. Usage.ai is built for multi-account and multi-organization setups. All analysis, recommendations, and approvals work across entire cloud footprints, including AWS, Azure, and GCP.

12. How is Usage.ai priced?

Usage.ai charges only on realized savings and not subscriptions or platform fees. For EC2 commitments, the fee is approximately 20% of savings; it may be higher for more complex workloads like databases. If you save $0, you pay $0.

13. Can Usage.ai help if my usage is highly unpredictable?

Absolutely. Flex Commitments were designed for volatile or fast-changing environments. The combination of daily optimization and real cashback makes unpredictable usage patterns safe to commit against.

Share this post

.png)

.png)